divinetutors13@gmail.com

divinetutors13@gmail.com

The Introductory Econometrics introduces students to the econometric methods used to conduct empirical analysis in Economics. The course is designed to provide the students with the basic quantitative techniques needed to undertake applied research projects. It also provides the base for more advanced optional courses in econometrics.

Course Modules:

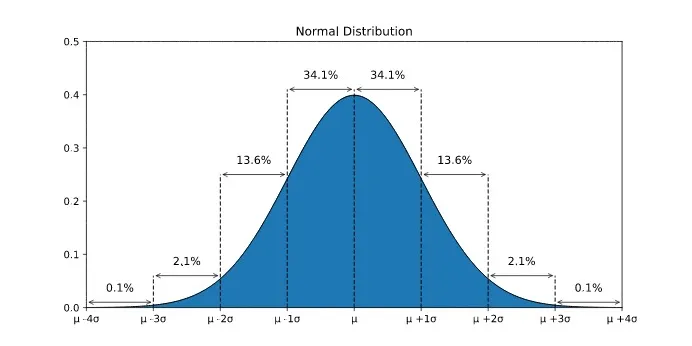

Normal Distribution, Z and t distribution, Chi-square distribution and F- Distribution

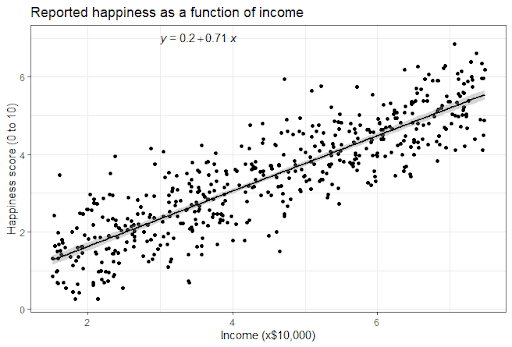

Ordinary least squares estimation of a linear model; properties of estimators; goodness of fit; testing of hypotheses; scaling and units of measurement; confidence intervals; the Gauss Markov theorem; forecasting and prediction

Extension of the single explanatory variable case to a multivariate setting; introducing non-linearities through functions of explanatory variables.

Multicollinearity; heteroscedasticity; serial correlation

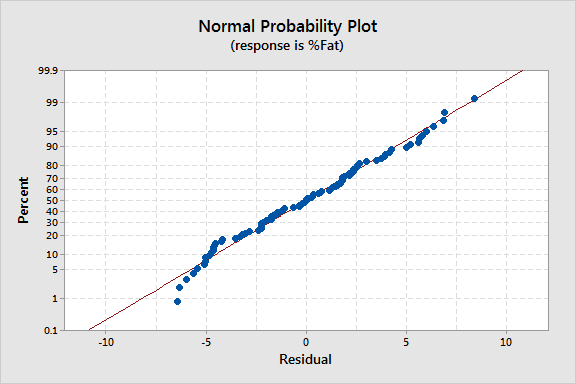

Omission of a relevant variable; inclusion of irrelevant variable; specification tests

NOTE: The above modules give a rough idea about the topics covered in our Introductory Econometrics course. Students will be given modules as per their respective University’s outline after prior discussion. dseonline