divinetutors13@gmail.com

divinetutors13@gmail.com

In the Financial Economics course, Students acquire extensive theoretical knowledge in portfolio risk management, capital asset pricing, and the operation of financial derivatives. The course familiarizes students with the terms and concepts related to financial markets and helps them comprehend business news/articles better. It also helps to enhance a student’s understanding of real-life investment decisions. The course has a strong employability quotient given the relatively high demand for skilled experts in the financial sector.

Deterministic cash flow streams; basic theory of interest; discounting and present value; internal rate of return; evaluation criteria; fixed-income securities; bond prices and yields; interest rate sensitivity and duration; immunization; the term structure of interest rates; yield curves; spot rates and forward rates

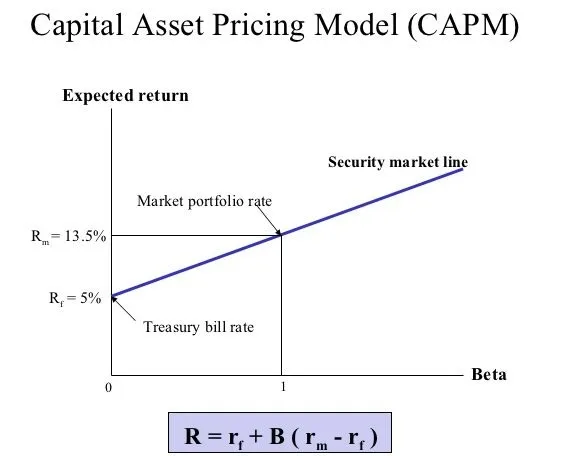

Single period random cash flows; mean-variance portfolio theory; random asset returns; portfolios of assets; portfolio mean and variance; feasible combinations of mean and variance; mean-variance portfolio analysis: the Markowitz model and the two-fund theorem; risk-free assets and the one-fund theorem. CAPM: the capital market line; the capital asset pricing model; the beta of an asset and a portfolio; security market line; use of the CAPM model in investment analysis and as a pricing formula; the CAPM as a factor model, arbitrage pricing theory

Introduction to derivatives and options; forward and futures contracts; options; other derivatives; the use of futures for hedging, stock index futures; forward and futures prices; interest rate futures and duration-based hedging strategies, options markets; call and put options; factors affecting option prices; put-call parity; option trading strategies: spreads; straddles; strips and straps; strangles; the principle of arbitrage; discrete processes and the binomial tree model; risk neutral valuation; stochastic process (continuous variable, continuous time), the Markov property, Itô’s lemma; the idea underlying the Black Scholes-Merton (BSM) differential equation, BSM pricing formulas; the Greek letters

NOTE: The above modules give a rough idea about the topics covered in our Financial Economics course. Students will be given modules as per their respective University’s outline after prior discussion. dseonline